When it comes time to sell your company, the decision to hire an investment banker is not always the best one. In the right circumstances, however, a banker can add value to your sale process. If you and your board have decided to hire a banker, it is in your advantage to ensure that the fee or engagement letter that you get in place is fair and even favorable to the company. At the same time, it is also important to properly incentivize your banker. Here are some suggestions:

- Don’t rush into getting a fee letter in place.

It is natural for a banker to push to formalize the relationship (and fee), but there is little upside for you to do this early. I have seen smaller company CEOs make this mistake and succumb to the pressure several times. Larger, more sophisticated companies, on the other hand, rarely make this mistake. Although the preparatory work to sell the Company will begin well in advance, the right time to get the letter in place is just before you begin formal outreach to various buyers.

There are several advantages for you to do this. If you formalize the relationship before you have seen the banker’s work and had a chance to really evaluate the individuals working on the assignment, and you subsequently decide to switch banks, this can be a painful process. Even if they are terminated, the precedent bank will usually have the right to a fee if a transaction takes place within a certain time frame, and this need to pay a “double fee” will be expensive and will inhibit your ability to hire a new bank. Additionally, you will likely get better service from your banker when they are still working to earn the mandate.

- Promote competition.

Even if you have a preferred bank in mind, I recommend that you invite 2-3 other banks to pitch for the business. To the extent you are having legitimate conversations with other banks, this competitive dynamic will introduce fee pressure into the negotiation. Additionally, as I mention above, you often get the various banks best thinking before the hiring decision is made.

- Request (multiple) “fee comps.”

Entrepreneurs rarely ask for a fee comp, and many don’t know what it is. A fee comp is simply a list of precedent transactions that your banker will produce that includes pertinent information such as: the size of the transaction (enterprise and equity value), dollar amount of fees paid, % of equity value, and list of bankers that worked on the deal. Usually, it is appropriate to sort and only include deals in the same or similar industry as yours and those of a similar expected value range. It is a useful sanity check that allows you to verify if your deal fee is consistent with the median fee. Additionally, I would recommend requesting several fee comps from other banks as well. To the extent there is significant difference, you can introduce further competitive tension by pointing to the lower comp set or having your preferred bank add relevant deals with lower fees that may have been excluded.

- No retainer fees.

Of all the terms bankers sometimes try to negotiate into letters with entrepreneurs, this is the one I hate the most. Here, a bank will try to ensure that they get paid regardless of the outcome of the sale process. Entrepreneurs sometimes agree to this because they think it is standard. For a simple sale process, it is not standard, and if your banker insists on this term, it should be a red flag for you. Unless it is an ongoing advisory assignment like a raid defense, even banks such as Goldman Sachs and Morgan Stanley will not typically ask for a retainer fee.

In the event that, usually a boutique bank, will not step off the retainer construct and you still believe they are your best option, make sure that any retainer paid is creditable against the final success fee.

- Decrease the minimum fee and provide a generous incentive fee if your desired price is surpassed.

If a banker asks for a minimum fee, try to lower that amount. In exchange, propose to increase the fee (as a percentage) if the business sells at the high end of your range. This sliding fee scale will effectively incentivize your banker to get the highest price.

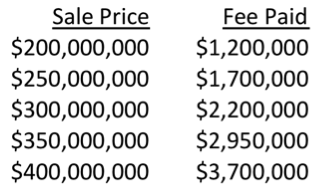

For example, let’s say you, your investors, and bankers believe the fair market price of your business is $300 million. The minimum price you would be willing to sell the business is $200 million, and a valuation you would be very happy with that is possible but would be a stretch to achieve is $400 million. In this case, a hypothetical fee construct could be:

- $1 million minimum fee

- 60bps up to $200 million

- 100bps on increment above $200 million up to $300 million

- 150 bps on anything above $300 million

- Have a reasonable expense cap.

Unless there are clear expenses you know of, it should probably be $10,000 or less.

- Be fair.

One last note. While it is important to settle on a fee construct that is fair, and perhaps even favorable to you, you need to be careful about cutting it too close. If the fee is too anemic, your banker will not be engaged or your deal will get staffed with the B team. The key is to determine a fair fee and incentivize and reward your banker to help you get the highest price for your business.

Copyright 2015 Ali Rahimtula. All rights reserved.