Institutional venture capital investors generally prefer to do priced rounds as opposed to investing in convertible notes. Nevertheless, these securities (be they SAFEs or convertible notes) are and will likely continue to be common among early-stage companies. Having been an investor in some of these notes and more often an investor in the first priced round in a company with existing notes, I thought it would be useful to write about how these notes can be treated in your Series A. It is a subject that entrepreneurs sometimes have difficulty with because of a lack of familiarity. The topic is important because the note treatment can change the effective Series A price and have a real impact on founder dilution.

A Quick Primer on the Conversion Mechanism

A note can have a discount rate, a valuation cap, or both. These determine the note conversion price, which, when divided into the capital raised from the notes, gives the number of shares issued. Our illustrative example below has both a cap and a discount rate since this will also show how note securities with just one or the other work too. A simple explanation of these terms is below:

- Conversion price: the lower of the valuation cap price and the discount price.

- Valuation cap price: (valuation cap) / (shares outstanding prior to the equity issuance[1]).

- Discount price: price per share of Series A issuance * (1 – discount rate).

How Notes Are Treated in the Series A: Three Cases

The founders, existing investors, and new Series A investor will generally negotiate and decide how the notes convert upon the Series A investment. There are, broadly speaking, three ways to do this, enumerated below.

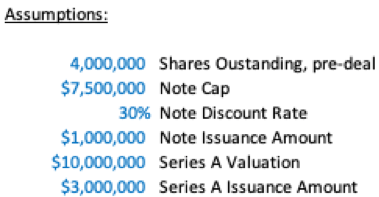

After each methodology, I’ll provide an illustrative example. The scenario we will examine is of a company with $1mm of notes outstanding with a $7.5mm valuation cap and a 30% discount. Management is raising a $3mm Series A with a headline valuation of $10mm.

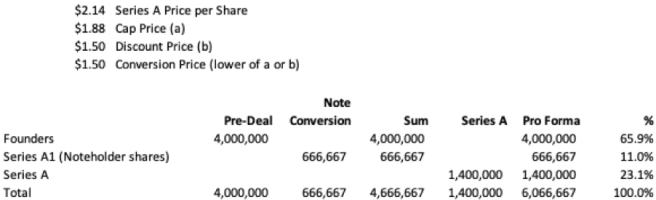

Case 1: Notes convert prior to the Series A investment. This is sometimes called the “percentage ownership method.” The notes convert into a series of Preferred shares (let’s call them A1 shares), which dilutes the founders. Then after this, the Series A is issued, which dilutes the founders and the former note holders.

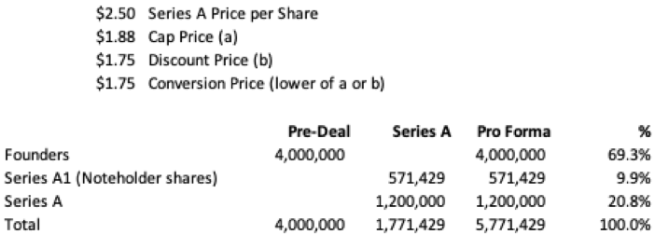

Case 2: Notes convert into the Series A. This is sometimes called the “pre-money method.” This has the effect of diluting the new money, i.e., the issuance of shares related to the old notes dilutes the new money ownership.

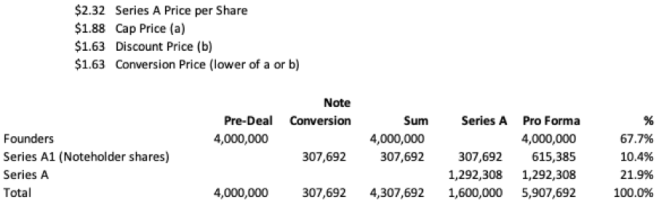

Case 3: A split between 1 and 2. You can convert some of the notes before the new investment and put the rest into the round. The illustrative example below splits it 50%/50% (but any split can be negotiated). Obviously, this will have a dilution impact on the founders and Series A investors in between cases 1 and 2.

Real Implications

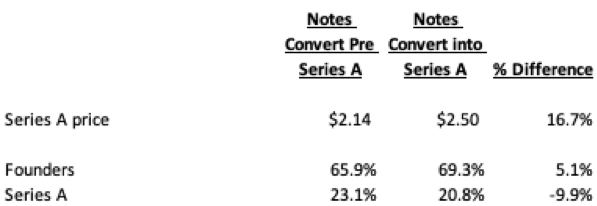

As shown below, the economic difference between the cases is real. The first implication is that the Series A price is almost 17% different between the first two cases. This reinforces the importance to focus on price per share rather than the headline price of $10mm. Second, there is a significant impact on pro forma ownership. The ownership difference is 10% lower for the Series A investors and 5% higher for the founders. These differences are shown in the table below.

Conclusion

At first blush, it may seem that case 1 is unfair to founders. This is not necessarily so. There are cases when companies have several classes of notes stacked on top of each other which in aggregate can be significant. Additionally, there can be notes with low caps (i.e. severe discounts to the Series A price) that result in large share issuances. It can also be argued that cash raised from the notes has been spent and it would be unfair for the new money coming in to be diluted by it.

Either way, Series A investors will view treatment of the notes as one lever to get their desired pro forma ownership percentage. One could just as easily lower the Series A issuance price to achieve this objective. Just as with price, the way the notes are ultimately treated comes down to the competitive tension in the round and the negotiating leverage you have in your raise. The important thing is for you to be aware of the real dilution impact the note conversion will have for you, and to focus on that rather than the round’s headline price.

[1] In our example, we exclude the impact the note conversion in the company capitalization. Some note documentation specifies that company capitalization includes the note conversion.

Ali, very informative. This is an area that I’m weak in. Would you mind sharing the spreadsheet? It’d helpful to understand the calculations.

LikeLike

Sure Ben. Just sent to you. I hope it is useful.

LikeLike