Note: This post was written in August 2019. WeWork (referenced in the last paragraph) subsequently pulled its IPO in late September 2019, largely because investors came to view it as a property management firm rather than a technology company. I believe what played out with WeWork largely corroborates the thesis of this post.

In my work as a venture capital investor, I often meet companies that position themselves as technology firms but whose core product or business is similar to traditional incumbents. In many cases, they may use technology to deliver their product more efficiently, but they are not selling technology, and often they are not fundamentally innovating the product they are selling.

For example, in the financial technology sector, at a high-level, I can bisect the universe into (1) true technology companies that sell software or data to financial institutions, and (2) technology-enabled financial services companies.

This begs the question, how should the second category of companies be valued? Should they trade at a premium valuation – like real technology companies? Or are they more akin to “false fintechs” that, over time, trade like banks and insurance companies?

Before we answer this question, I would note that this second category of companies can be very strong (and can make for excellent investments.) On Deck, an example used below, is an online small-business lending company that was one of the most successful startups to ever go public from the New York City venture-backed ecosystem. And there are several others. Furthermore, to state the obvious, traditional financial institutions are among the largest and most successful companies in our economy (as of this writing, JP Morgan Chase has a market cap in excess of $340 billion, and Berkshire Hathaway has a market cap approaching $500 billion, for example).

The data exhibit below shows the price/revenue (last 12 months) multiples for three comp sets:

- Traditional financial institutions. These include companies like Citigroup and Wells Fargo.

- True technology companies that sell into the financial services sector. They take little, if any, balance sheet risk. They include companies like Guidewire, which sells policy administration software to the insurance industry, Fidelity National Information Services, which sells core banking software to banks, and MasterCard, which provides payments rails.

- Tech-enabled financial services firms. These include firms like On Deck, Lending Club, and Greensky, which take balance sheet risk. It also includes excellent companies like Progressive, which sells auto and property insurance largely online and has services its customers digitally.

Note: Trading prices as of August 15, 2019.

As you can see, the true technology companies trade at a median of 10.1x revenue, over ten times the multiples of the tech-enabled financial services companies. In this sense, one can consider them to be “false fintechs.” We can theorize that this is because, in addition to higher growth, the technology companies have higher quality and more predictable revenue. Specifically, they more likely have subscription-based revenue rather than transactional revenue. They also have a more defensible moat because the technology they sell is very hard to build.

It is interesting that the traditional financial institutions also trade almost two turns higher as well. Why is that? They are more valuable because, in addition to having some of the strongest brands in our economy, these companies in this category also benefit from scale advantages.

Furthermore, many of these traditional financial institutions extensively use technology to operate their business. I recently read a presentation from JP Morgan pitching treasury services to one of my portfolio companies, and the amount of non-balance sheet fee income they generate is impressive. Their services included secure credentials distribution, host-to-host file transmission, file tracking capabilities, various analytical reports, and many others. Many Wall Street banks have Blockchain groups have innovated with several Blockchain patents. Goldman Sachs even employs more software engineers than investment bankers.

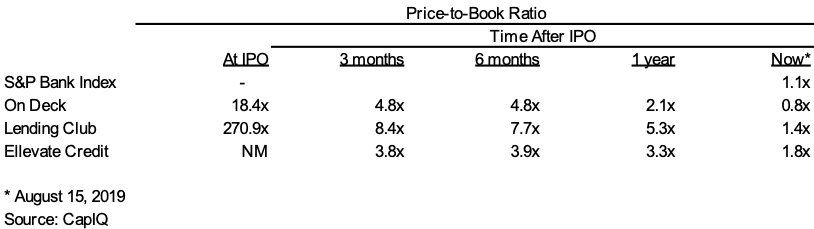

It is very illuminating to examine the way the false fintechs trade over time.

Note: Trading prices as of August 15, 2019.

In the rather staggering exhibit above, you can see that they tend to trade at very high multiples at IPO, and then tend to come down over time. There are some dramatic examples of this. According to CapIQ, at IPO, Lending Club traded at a Price/Book in excess of 270x, On Deck over 18x, and Ellevate Credit around 4x. Over time these multiples have trended down. Today they trade similarly to the S&P Bank Index.

What accounts for this inflated valuation at IPO? There could be some misunderstanding in the marketplace because investors perceive these companies to be technology companies when, in fact, their primary business is really more similar to a bank. Additionally, it must be noted – as shown in the exhibit below – at IPO, they all had robust growth expectations. Not surprisingly, when growth slows down, the multiples come down.

Note: Trading prices as of August 15, 2019.

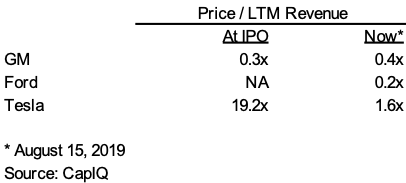

Is this phenomenon applicable to other sectors beyond financial services? Absolutely. Take a look at Tesla’s price performance relative to GM and Ford. According to CapIQ, Tesla traded at over 19x revenue at IPO vs. GM trading at 0.3x at its re-IPO. Today, Tesla trades at 1.6x, still a premium over GM and Ford but much less than before.

Note: Trading prices as of August 15, 2019.

It will be interesting to watch how other companies in the IPO pipeline will perform. Will WeWork trade like a technology company or a property management firm? Will Compass trade like a technology company or a real estate brokerage firm? What they have built is unquestionably impressive. But will premium valuations over traditional competitors will be durable? Time will tell.

Appendix – Comp Group Constituents

Note: Trading prices as of August 15, 2019.

Acknowledgements: I would like to thank Karen Robinson-Rafuse for her contributions to this piece.